The IEA Weighs in

The best bits of the International Energy Agency's new report

If you saw me sitting motionless for three hours in a DC café this morning, it was because I was reading the International Energy Agency’s new report, “Key Questions on Energy and AI.” This report follows their first on the subject, “Energy and AI” (2025), which I was fortunate enough to advise and peer review while at the State Department.

The report puts numbers behind some of the biggest trends in AI and energy from the past year—in finance, electricity, and policy. Here are some things that stood out to me:

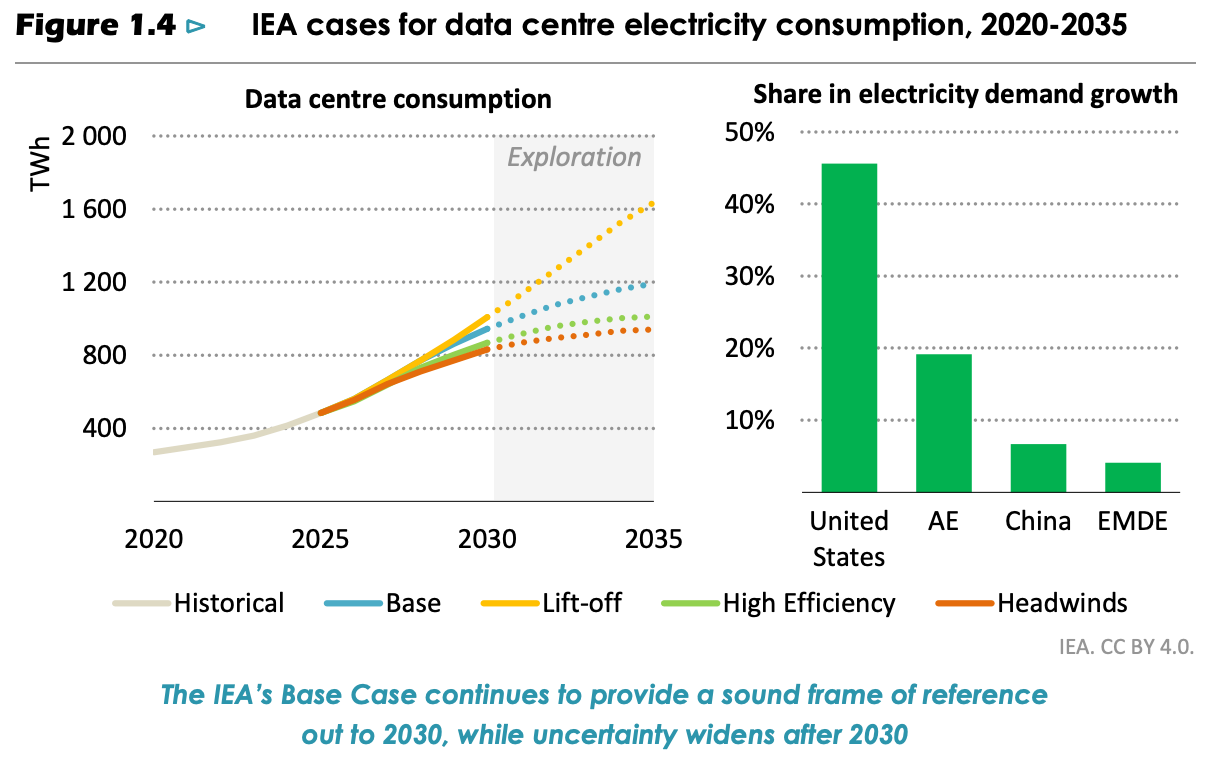

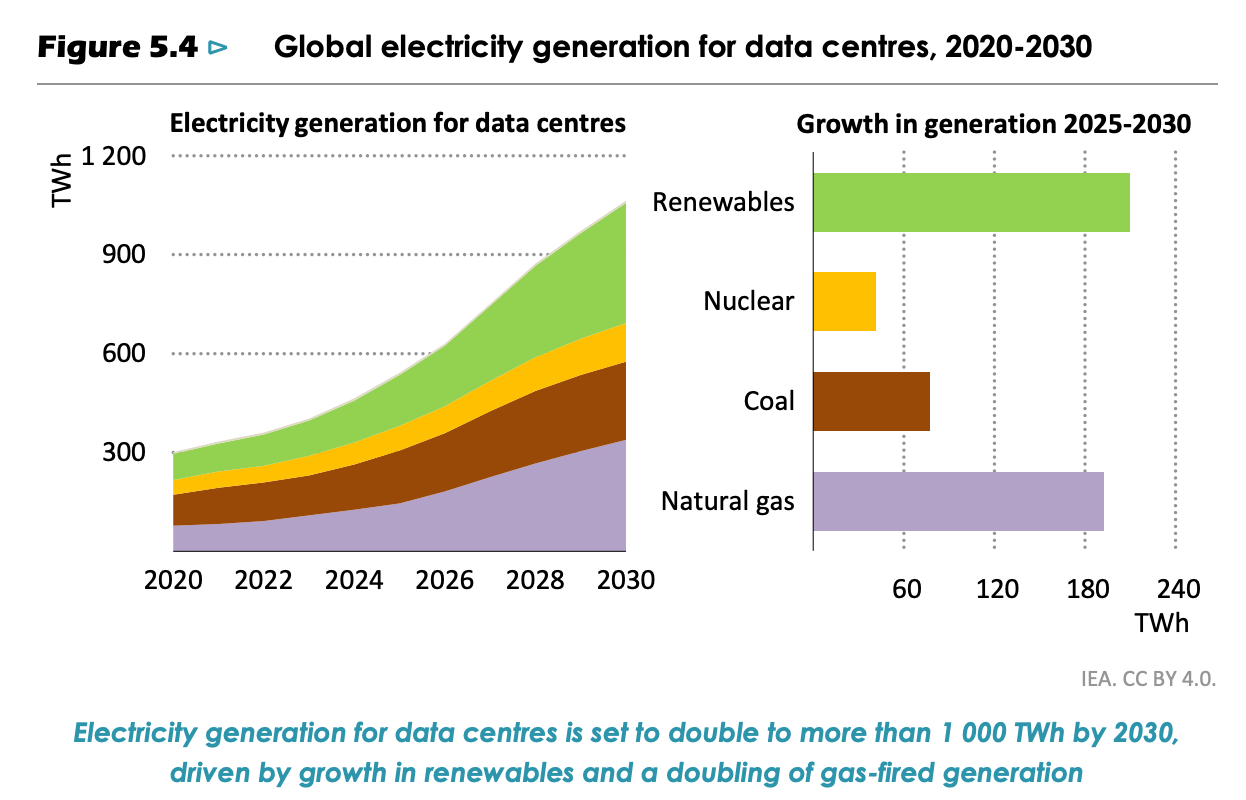

AI boom holds steady: In 2025, the IEA projected that data centers would consume 945 TWh by 2030. This year, they upped that marginally to 950 TWh, signaling that the demand fundamentals that drove the AI boom in 2025 remain strong. Notably, the only significant revision to their forecasts was to scale back the “lift-off” case in the near term, owing to physical constraints on data center buildout that the IEA expects will ease later on.

Southeast Asia growing fast: Southeast Asia remains a major growth region for data centers, with over 6 GW of planned capacity. All eyes are on Malaysia as the fastest-growing market in the area.

Inference, nearby: Two separate trends could reveal something about the data centers of the future. First, the IEA notes, “The balance of AI-related energy consumption has already shifted decisively from training to inference.” Second, the report highlights the persistent tendency of data centers to cluster around population centers and fiber networks. Taken together, these trends could point towards a future of relatively modest-sized data centers clustered around cities, rather than GW-scale training campuses in the middle of nowhere. Projects like Stargate will still grab the headlines, but they likely won’t be representative of the industry.

Per-query energy use: The good news is we now have pretty good data on how much electricity a single chatbot query consumes (~0.34 Wh/query for the frontier models). The bad news is that it’s telling us less and less about AI’s overall energy demand. As the uses of AI diversify, chatbot queries are accounting for a smaller portion of overall demand—and we don’t have a good idea of how much energy those other uses (such as autonomous agents, enterprise models, or video generation) require.

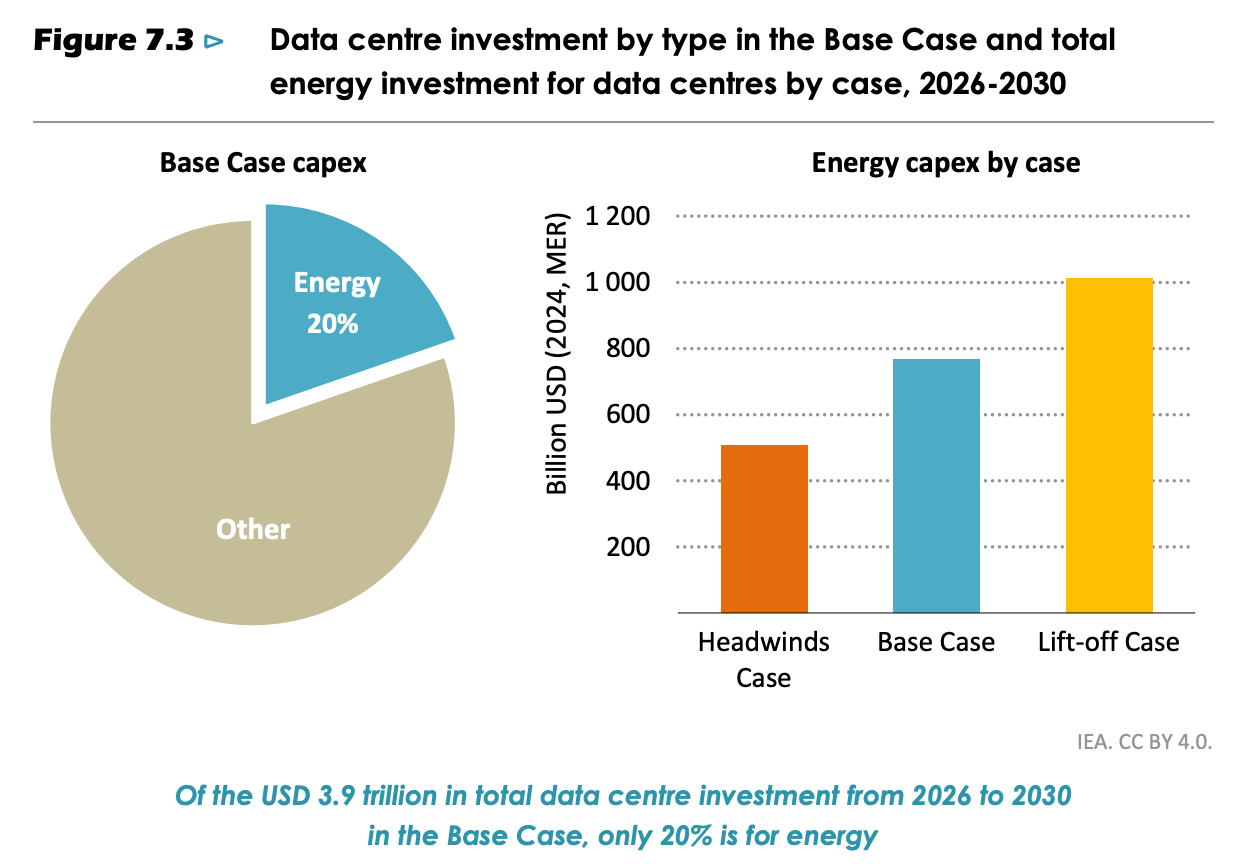

A committed, but not exclusive, relationship: There’s no doubt that data centers and energy are inextricably intertwined. But the IEA’s data shows that data centers aren’t the only story in the energy industry—and energy isn’t the only story in the AI sector. Consider that data centers account for “less than 10% of electricity demand growth globally to 2030.” Or that natural gas turbine orderbooks are heavily backlogged, but that data centers were “not the direct cause” of this demand surge. Or that energy is likely to account for only 20% of data center-related capital expenditures through 2030. AI is a big deal for the energy system, but it’s not the only game in town.

Challenging customers: A persistent challenge with data centers is the unpredictability of their power demand. With many tasks running synchronously, it is not unusual to see dramatic fluctuations in data centers’ power draw, which, as Jigar Shah recently noted on the podcast Volts, is not an activity grid operators typically allow large electricity customers to engage in because of the danger it poses to the grid. As more data centers connect to the grid, this is going to be a major headache for grid operators—and a real risk to grid stability.

All signs point to batteries: Batteries seem poised to emerge from the AI age as a winner. They perform a number of valuable services for data centers, including improving power supply reliability, augmenting generation from variable renewable energy, and accommodating the aforementioned demand swings. (They will also be needed if manufacturers are to switch to AI-enabled robots.) The IEA projects that 20-25 GW of battery storage could be installed at data center sites by 2030.

PPAs reign supreme: Despite a proliferation of new power procurement tools, power purchase agreements remain the dominant avenue buying electrons. By 2027, they are likely to cover more than half of data center electricity demand, with the United States accounting for the plurality of contracted volume.

Affordability impact muddled: The IEA found that data centers can be a boon or a bust for electricity affordability. High load factors (ratio of average load to peak load) mean they could improve affordability by paying for a lot of electricity without necessitating too many grid upgrades. But uncertainty about ramp rates, cost allocation, and utilization can just as easily push in the other direction. Ultimately, whether data centers increase or decrease your electricity bills will come down to policy and planning.

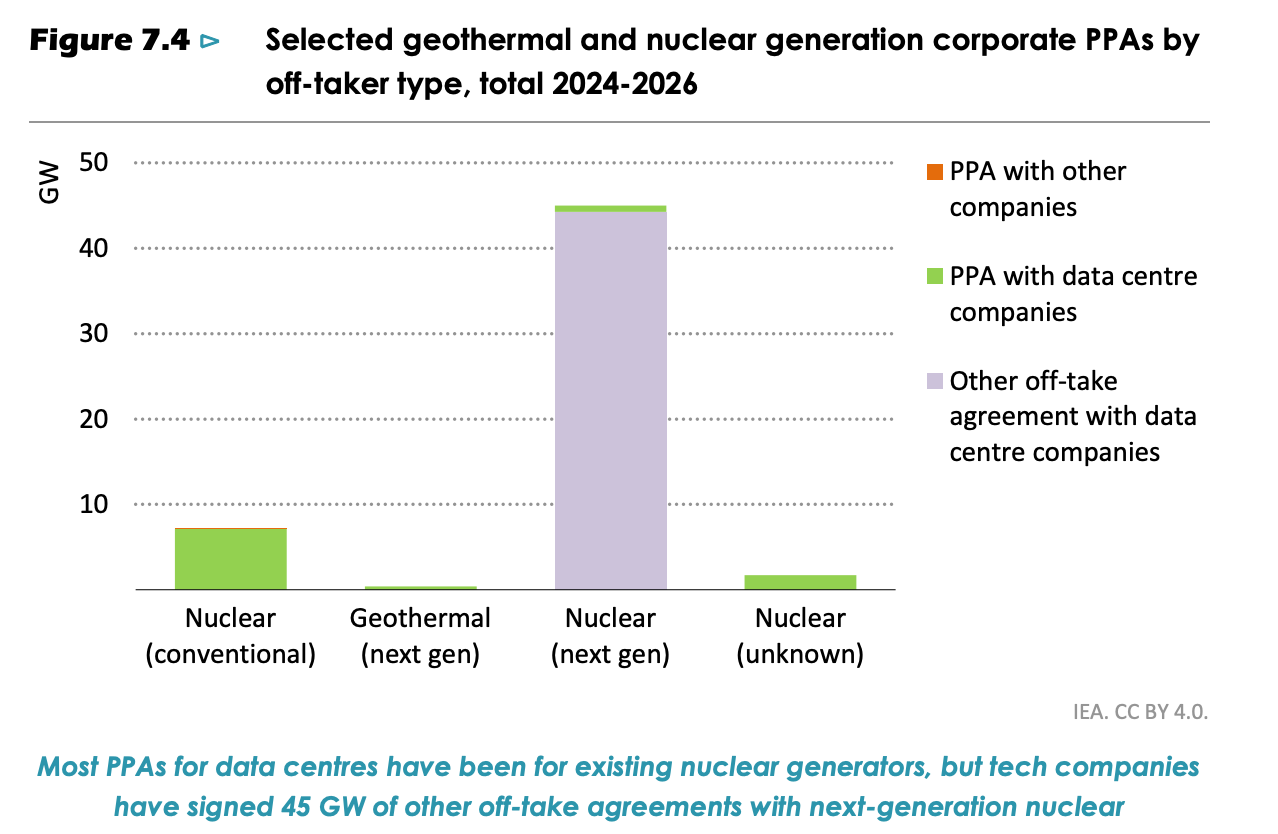

Tailwinds for clean firm power: Data centers’ energy demand has provided a boost to emerging clean firm power technologies, specifically SMRs and advanced geothermal. There is now 45 GW of contracted SMR capacity. The other side of this coin is that both industries would be significantly harmed by a contraction of the AI industry.

Onsite power’s challenges: 70 GW of onsite capacity has been proposed at data centers, but only 5.6 GW is currently under construction, and it’s nearly entirely in the United States. The IEA is cool on the effectiveness of behind-the-meter power, noting that it creates challenges for reliability, risks fuel bottlenecks, increases the need for overbuild, and raises overall cost.

Lead times, lean times: Lead times for transformers (2-3 years), gas turbines (5 years), and high-end memory (1-2 years) are critical bottlenecks for data center developers. But manufacturers are being cautious about building out too much new capacity in the short term. Expect a modest scale-up in existing factories, but not too many new ones.

Second-order effects: AI’s impacts on energy demand won’t just come from data centers—it will come from how the technology reshapes the economy. Accelerated GDP growth from AI could increase global energy demand 0.9-2.6% by 2035, though AI-driven efficiencies and job losses could push in the other direction.

AI adoption in the power sector: AI adoption in the power sector could save 13.5 EJ (via efficiencies) by 2035, but broader adoption is being hampered by skill gaps and inadequate data availability, as well as utility incentives that do not favor energy efficiency.

East vs West on physical AI: While the United States remains the world leader in developing AI models, China is in the lead on incorporating AI into manufacturing. In this case, the signal is coming from the top, with the Government of China pushing companies to increase their uptake.